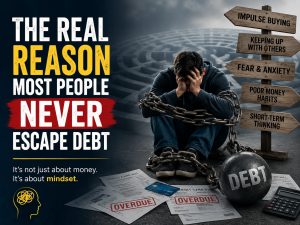

The Real Reason Most People Never Escape Debt

Many people assume debt is simply a money problem. Earn more, spend less, and everything will work out. But if that were true, why do some people with decent salaries still struggle with debt year after year?

Many people assume debt is simply a money problem. Earn more, spend less, and everything will work out. But if that were true, why do some people with decent salaries still struggle with debt year after year?

James, a 34-year-old professional, earned a stable income and received regular promotions at work. From the outside, his life looked successful. He drove a good car, wore designer clothes, and frequently upgraded his gadgets. Yet behind closed doors, he was drowning in loans, credit card balances, and unpaid bills.

Every month, James promised himself things would change. But whenever stress hit, he found comfort in online shopping. When friends posted vacations and achievements on social media, he felt pressured to keep up. And whenever his bank balance made him anxious, he avoided checking his statements altogether.

The problem was never just income. It was the hidden psychological patterns driving his financial decisions.

James’ story is not unique. Millions of people remain trapped in debt not because they lack intelligence or opportunity, but because emotions, habits, social pressure, and mental triggers quietly shape how they spend, borrow, and manage money.

Understanding these psychological factors is the first step toward breaking free from the cycle of debt and building lasting financial health

- The Role of Instant Gratification in Accumulating Debt

Instant gratification refers to the desire to experience pleasure or fulfilment without delay. This psychological phenomenon plays a significant role in why individuals may accumulate debt. When faced with the choice between immediate rewards, such as buying new gadgets or enjoying luxury experiences, and long-term financial stability, many opt for the former. This tendency can lead to overspending and, ultimately, financial trouble.

Furthermore, the rise of online shopping and easy credit options has made it even easier to satisfy immediate desires. The convenience of accessing funds can create a cycle of impulsive purchases, reinforcing the habit of prioritizing short-term pleasure over long-term financial health.

- Fear and Anxiety: Emotional Drivers of Financial Decisions

Fear and anxiety are powerful emotions that can significantly impact financial decision-making. For instance, the fear of missing out on opportunities or the anxiety of not keeping up with peers can drive individuals to make impulsive financial choices, such as accruing debt to maintain a certain lifestyle. This emotional response often leads to a pattern of borrowing that can spiral out of control.

Additionally, anxiety about financial stability can cause individuals to avoid addressing their debt issues altogether. This avoidance can result in a lack of financial planning and poor spending habits, further entrenching them in a cycle of debt.

- Cognitive Dissonance: How Our Beliefs About Money Influence Spending Habits

Cognitive dissonance occurs when individuals hold conflicting beliefs or attitudes, which can lead to unhealthy financial behaviours. For example, someone may believe that they should save money while simultaneously indulging in unnecessary purchases. This conflict can create stress, leading to rationalizations that justify overspending, such as convincing oneself that they deserve a treat after a tough week.

Moreover, this dissonance can result in a disconnect between financial goals and actual spending habits. By failing to align their beliefs with their behaviours, individuals may find themselves trapped in a cycle of debt that contradicts their financial aspirations.

- The Impact of Social Comparison on Financial Choices

Social comparison theory suggests that individuals determine their own social and personal worth based on how they stack up against others. In the context of finances, this can lead to unhealthy spending as individuals strive to match the lifestyles of their peers or celebrities. This pressure can result in overspending on items that may not be affordable, leading to increased debt.

Additionally, the influence of social media amplifies this tendency, as curated online personas often showcase an idealized version of life that may not reflect reality. The desire to project a similar image can lead to financial decisions that prioritize appearances over sound fiscal management.

6 Strategies for Overcoming Psychological Barriers to Financial Health

- Recognize Psychological Triggers

- Identify emotional and psychological factors that contribute to debt and poor financial decisions.

- Practice Mindful Spending

- Become aware of triggers that lead to impulsive purchases.

- Make intentional spending choices that align with long-term financial goals.

- Set Clear Financial Goals

- Define realistic short-term and long-term financial objectives.

- Use goals to stay motivated and financially disciplined.

- Create and Follow a Budget

- Develop a practical budget to track income and expenses.

- Reduce emotional and unplanned spending through structured financial planning.

- Seek Professional Support

- Consult financial advisors or debt counsellors Debtors Care WhatsApp for guidance.

- Gain accountability and expert strategies for overcoming harmful financial habits.

- Build Healthier Financial Habits

- Replace detrimental financial patterns with sustainable money management practices.

- Focus on achieving long-term financial security and stability.